Florida's No-Fault Insurance System Explained: What It Means for Florida Drivers in 2026

Learn how Florida's no-fault insurance system affects your rights after a car accident, including PIP coverage, serious injury thresholds & changes.

.webp)

Riley Beam

- Florida's no-fault insurance system requires your own PIP coverage to pay for medical expenses and lost wages regardless of who caused the accident, but this coverage is limited to eighty percent of medical bills and sixty percent of lost wages up to ten thousand dollars.

- You must seek medical treatment within fourteen days of an accident to qualify for PIP benefits in Florida, or you risk losing all coverage despite paying premiums.

- To pursue compensation beyond PIP limits, including pain and suffering damages, your injuries must meet Florida's "serious injury threshold" by qualifying as permanent, causing significant scarring, or resulting in loss of an important bodily function.

Worried About Your Injury Case? We'll Review It - Free!

Imagine driving through Melbourne when suddenly—crunch!—someone rear-ends your car at a stoplight. Your neck hurts, your car has a dented bumper, and now you're wondering: "Who's going to pay for all this?" In Florida, the answer might surprise you.

Florida is one of only 12 states that operates under what's called a "no-fault" insurance system. But what does "no-fault" actually mean for you as a driver? Despite what the name suggests, it doesn't mean that nobody is blamed for the accident. It simply means that after a car crash, you turn to your own insurance company first to pay for your medical bills, regardless of who caused the accident.

Here's where many people get confused: the "no-fault" part only applies to injury claims—not vehicle damage. If someone crashes into your car, their insurance still pays for your vehicle repairs if they were at fault. Only your medical expenses and lost wages are handled differently under the no-fault system.

In Florida, every driver must carry two types of insurance:

- Personal Injury Protection (PIP): $10,000 minimum

- Property Damage Liability (PDL): $10,000 minimum

Your PIP coverage works like this: If you're hurt in an accident, your insurance company pays 80% of your necessary medical expenses and 60% of your lost wages, up to your policy limit (usually $10,000).

For example, if you have $8,000 in medical bills after an accident, your PIP insurance would typically cover $6,400 (80% of $8,000). You would be responsible for the remaining $1,600—unless you have health insurance or meet certain criteria to pursue the other driver for these costs (more on that later).

One important fact many Melbourne drivers don't realize: Florida's $10,000 PIP requirement hasn't increased since the 1970s. Medical costs have skyrocketed since then, meaning this coverage often falls short for accident victims with significant injuries. A single emergency room visit can easily exceed $10,000 today.

If you've been in an accident in Melbourne, understanding how this system affects your rights is crucial. Our Melbourne car accident attorneys can help you navigate the complexities of Florida's no-fault system and ensure you receive the compensation you deserve.

How PIP Insurance Works After Your Melbourne Car Accident

After a car accident in Melbourne, the clock starts ticking immediately on your insurance claim. The most critical deadline to remember is this: You must seek medical treatment within 14 days of your accident to qualify for PIP benefits. Miss this window, and your insurance company can deny your claim entirely—even though you've paid premiums for this coverage.

Let's walk through the PIP claims process step by step:

- Report the accident to your insurance company as soon as possible (ideally within 24 hours)

- Seek medical treatment within 14 days from a qualified provider

- Complete your insurance company's PIP claim forms

- Provide medical documentation and bills to your insurer

- Submit proof of lost wages if you missed work (requires documentation from your employer)

- Respond promptly to any additional information requests from your insurer

While this sounds straightforward, many Melbourne drivers encounter challenges during this process. Insurance companies may delay claims, request independent medical examinations (which often favor the insurer), dispute whether treatments were necessary, or claim your injuries were pre-existing.

What happens when your medical bills exceed your PIP coverage? For many accident victims, this happens quickly. After PIP benefits are exhausted, your health insurance typically becomes the next payer for ongoing treatment. If you don't have health insurance, you may become personally responsible for these costs—unless your injuries qualify you to pursue a claim against the at-fault driver (which we'll cover in the next section).

At Douglas R. Beam, P.A., we always encourage clients to work with their preferred medical providers, though we can provide guidance on which local Melbourne facilities commonly work with PIP claims if needed.

One of the most important things you can do to protect yourself after an accident is to keep detailed records of everything:

- All medical appointments and treatments

- Conversations with insurance adjusters (date, time, who you spoke with)

- Days missed from work

- Receipts for any out-of-pocket expenses related to your injuries

- Pain levels and how your injuries affect daily activities

These records become invaluable if your PIP benefits are unfairly denied or if your case eventually qualifies to pursue compensation beyond the no-fault system.

For assistance navigating these complex insurance matters, our Melbourne personal injury lawyers can provide guidance specific to your situation.

When Can You Sue Beyond Florida's No-Fault System?

Florida's no-fault system puts strict limits on when you can sue another driver after an accident. However, these limitations don't apply in all cases. The law includes what's called a "serious injury threshold" that, when met, allows you to step outside the no-fault system and pursue compensation directly from the at-fault driver.

Think of the serious injury threshold as a gateway. On one side is the no-fault system, where you're limited to your own PIP coverage. On the other side is the ability to seek full compensation from the driver who caused your accident, including pain and suffering damages that PIP doesn't cover.

To pass through this gateway, your injuries must qualify as "serious" under Florida law. This means you must have suffered at least one of these conditions:

- Significant and permanent loss of an important bodily function

- Permanent injury within a reasonable degree of medical probability

- Significant and permanent scarring or disfigurement

- Death

Let's make these legal terms more understandable with real-world examples:

Injuries that typically DON'T meet the threshold:

- Whiplash that heals within a few months

- Bruises and minor cuts

- Sprains that fully heal

- Temporary neck or back pain

Injuries that often DO meet the threshold:

- Herniated discs requiring surgery

- Fractures resulting in permanent mobility limitations

- Traumatic brain injuries with lasting effects

- Severe burns causing permanent scarring

- Injuries requiring joint replacement

Even when your injuries don't meet this threshold, you can still pursue the at-fault driver for economic damages that exceed your PIP coverage, such as medical bills and lost wages beyond the $10,000 limit. However, you cannot seek compensation for pain and suffering without meeting the serious injury threshold.

Meeting this threshold often becomes a contested issue. Insurance companies frequently claim injuries aren't permanent or serious enough to qualify. This is where expert medical testimony becomes vital—doctors must confirm that your injuries meet the legal standard of "permanent" or resulted in significant scarring or loss of function.

A 2018 Florida Supreme Court case (Progressive Select Insurance Co. v. Florida Hospital Medical Center) provides some help to accident victims by ensuring that PIP insurers must pay the full 80% of medical charges up to the policy limit without applying fee schedules that reduce payments. This helps maximize the benefits available under your PIP coverage.

If your injuries do qualify as serious under Florida law, you gain the right to pursue both economic damages (all medical bills, full lost wages, future medical costs) and non-economic damages (pain and suffering, emotional distress, loss of enjoyment of life) from the at-fault driver.

To learn more about whether your specific injuries might qualify you to step outside the no-fault system, contact our experienced truck accident lawyers for a personalized evaluation of your case.

How Florida's Comparative Negligence Law Affects Your Car Accident Claim

When accidents happen, fault isn't always black and white. Often, both drivers share some responsibility. This is where Florida's "comparative negligence" law comes into play—and it underwent a significant change in 2023 that every driver should understand.

Previously, Florida operated under a "pure comparative negligence" system, where you could recover damages even if you were 99% at fault (though your recovery would be reduced by your percentage of fault). Now, Florida uses a stricter "modified comparative negligence" standard with a critical 50% threshold.

Here's what this means in simple terms: If you're found to be more than 50% responsible for causing an accident, you cannot recover any damages from the other driver. This is a dramatic change that makes fault determination more important than ever.

Let's look at a real-world example:

Imagine you're in an accident with $100,000 in damages (medical bills, lost wages, pain and suffering). If you're found to be 30% at fault and the other driver 70% at fault, you could recover $70,000 (your damages minus your 30% responsibility). But if you're found to be 51% at fault—just 1% over the threshold—you recover nothing at all.

How is fault determined in Florida accidents? Several factors come into play:

- Police reports and traffic citations

- Witness statements

- Photos and videos of the accident scene

- Traffic laws that were violated

- Expert accident reconstruction

- Vehicle damage patterns

- Statements from both drivers

Insurance companies have a strong financial incentive to shift more blame to you. If they can push your fault percentage above 50%, they pay nothing. Even if they can't cross that threshold, every percentage point of fault they assign to you reduces what they have to pay.

This 50% rule makes having experienced legal representation more important than ever. Without proper advocacy, you might be incorrectly assigned too much fault, potentially costing you your entire claim.

The evidence collected in the immediate aftermath of an accident often proves decisive in these fault determinations. Our Melbourne car accident lawyers can help ensure all evidence is properly preserved and presented to protect your right to fair compensation.

Failed Attempts to Change Florida's No-Fault System

Florida's no-fault insurance system has faced repeated legislative challenges, but ultimately remains intact. In the 2025 session, the Florida legislature considered bills (SB 1256 and HB 1181) that would have repealed the state's no-fault insurance system and eliminated PIP requirements entirely.

While HB 1181 initially gained momentum—advancing through a Florida House panel vote on March 27, 2025—the bill was ultimately "indefinitely postponed and withdrawn from consideration" on May 3, 2025, and the Senate companion, SB 1256, died in committee on June 16, 2025. This outcome aligns with Governor DeSantis' previously expressed opposition to repealing the no-fault system.

Lawmakers tried again in the 2026 session with Senate Bill 522 and House Bill 769, but those bills also died in committee on March 13, 2026. These are the most recent of many unsuccessful attempts to overhaul Florida's auto insurance framework, following failed bills in 2021, 2023, and 2025.

What Changes Were Proposed?

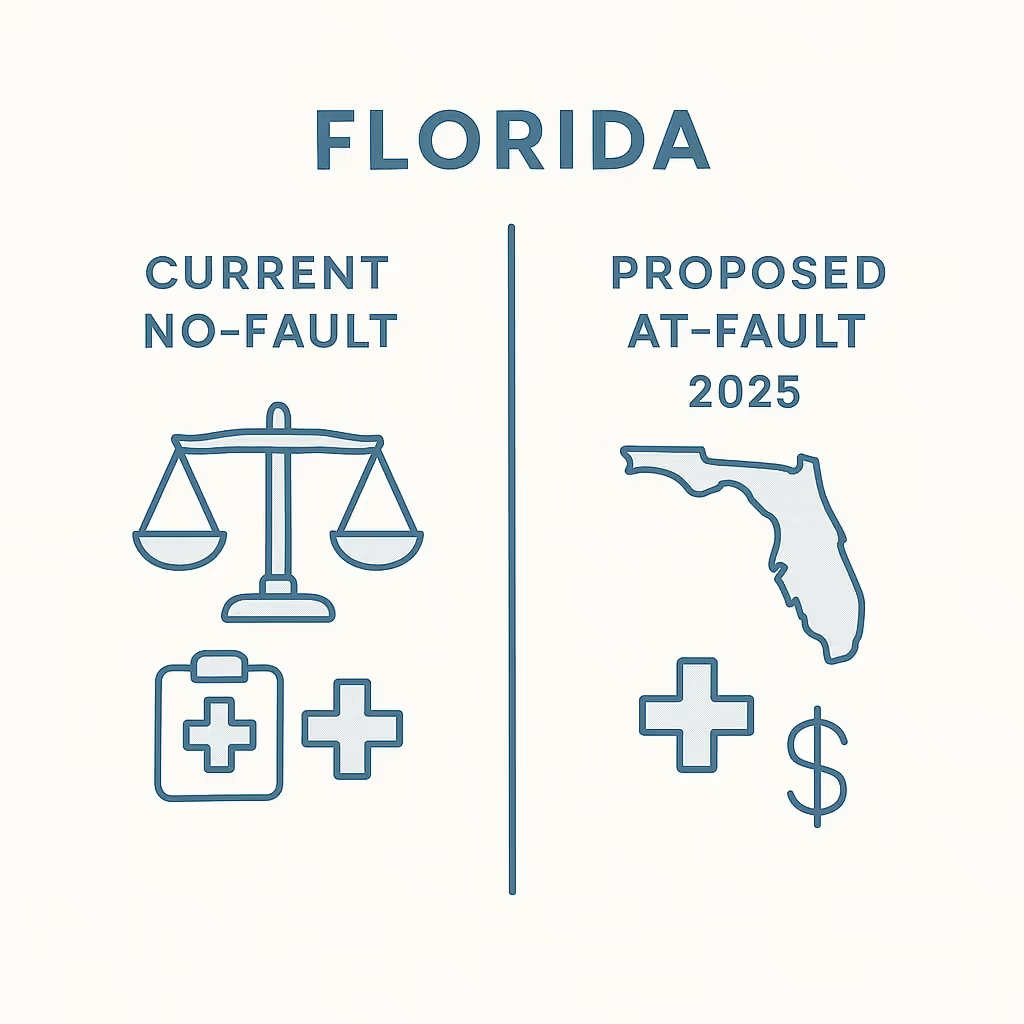

The proposed legislation would have dramatically transformed how Melbourne drivers handle accident claims. Here's how the proposed system would have compared to our current system:

Current No-Fault System:

- Required Coverage Types: Personal Injury Protection (PIP) + Property Damage Liability (PDL)

- Minimum Coverage Amounts: $10,000 PIP, $10,000 PDL

- Who Pays Medical Bills: Your own insurance pays first, regardless of fault

- When Lawsuits Are Allowed: Only if "serious injury threshold" is met

- Impact on Premiums: Lower premiums but limited coverage

- Main Advantage: Quick payment of medical bills without proving fault

- Main Disadvantage: $10,000 limit often insufficient for serious injuries

Proposed Fault-Based System (Not Passed):

- Required Coverage Types: Bodily Injury Liability + Property Damage Liability

- Minimum Coverage Amounts: $25,000/$50,000 Bodily Injury, $10,000 PDL

- Who Pays Medical Bills: At-fault driver's insurance pays

- When Lawsuits Are Allowed: For any injury caused by another driver

- Impact on Premiums: Potentially higher premiums but better coverage

- Main Advantage: Greater recovery potential for innocent victims

- Main Disadvantage: Requires proving fault, which can delay payment

What This Means for Melbourne Drivers

With the defeat of these repeal bills, Florida drivers will continue operating under the no-fault system for the foreseeable future. Here's what this means in practical terms:

- Continued PIP requirement: You must maintain $10,000 in Personal Injury Protection coverage

- No-fault medical claims: Your own insurance will continue to cover your medical expenses regardless of who caused the accident

- Serious injury threshold: The limitation on lawsuits remains—you can only sue the at-fault driver if your injuries meet Florida's "serious injury threshold"

- Property damage claims: Vehicle damage claims will continue to be handled on a fault basis

Given the stability of Florida's insurance requirements, Melbourne drivers should focus on:

- Understanding your current coverage: Ensure you know exactly what protection your policy provides under the continuing no-fault system

- Considering supplemental coverage: Since PIP's $10,000 limit remains inadequate for serious injuries, optional coverages like MedPay, collision, comprehensive, and especially uninsured/underinsured motorist coverage provide valuable additional protection

- Maintaining compliance: Keep proof of insurance and vehicle registration in your car at all times

- Consulting with professionals: If you're in an accident, seek advice from an experienced attorney who understands the nuances of Florida's no-fault system

To learn more about how Florida's insurance laws affect your rights after an accident, contact our car accident lawyers for guidance specific to your situation.

Key FAQs About Florida's No-Fault Insurance System

If I'm injured in a car accident in Melbourne, do I file a claim with my insurance or the other driver's insurance?

For your injuries, you first file with your own PIP insurance regardless of fault. This is the "no-fault" part of Florida's system. Your PIP coverage should pay 80% of your medical bills and 60% of lost wages, up to the $10,000 limit.

For vehicle damage, you file with the at-fault driver's PDL insurance. Vehicle damage claims still operate under a fault-based system, even in Florida.

If your injuries meet the serious injury threshold (permanent injury, significant scarring, or loss of important bodily function), you can then pursue a claim against the at-fault driver's bodily injury liability insurance for additional compensation, including pain and suffering.

What if the driver who hit me doesn't have insurance?

Unfortunately, Florida has one of the highest rates of uninsured drivers in the country. Roughly one in six drivers has no insurance at all. If you're hit by an uninsured driver, your own PIP will still cover your initial medical bills up to its limits.

However, once your PIP benefits are exhausted, you could be facing significant financial hardship without additional coverage. This is why uninsured/underinsured motorist coverage is so important, though not required in Florida. This optional coverage protects you if the at-fault driver has no insurance or inadequate coverage to pay for your damages.

Without this coverage, your options may be limited to filing a lawsuit directly against the uninsured driver (who may have limited ability to pay a judgment) or relying on your health insurance for ongoing medical care.

What if my medical bills exceed my $10,000 PIP coverage?

This happens frequently, especially with serious injuries. Once your PIP coverage is exhausted, your health insurance typically becomes the next payer for ongoing medical treatment. If you don't have health insurance, you may be personally responsible for these costs.

However, if your injuries meet the serious injury threshold, you can pursue the at-fault driver for medical expenses beyond what PIP covered. This includes future medical expenses related to your injuries.

Even if your injuries don't meet the threshold, you may still pursue the at-fault driver for economic damages (medical bills and lost wages) that exceed your PIP coverage—you just can't claim pain and suffering damages without meeting the threshold.

If I'm visiting Florida from another state and get in an accident, does the no-fault system apply to me?

If you're visiting Florida from a state that doesn't have no-fault insurance and get into an accident with a Florida driver, the situation becomes more complex. Generally, the laws of the state where the accident occurs (Florida) apply, but your out-of-state insurance may handle claims differently.

Visitors typically aren't required to have PIP coverage, so your claim would likely proceed under the liability coverage of your policy or the Florida driver's policy, depending on who was at fault. However, if you're staying in Florida for an extended period or are a seasonal resident, different rules may apply.

Do I need an attorney for a PIP claim in Florida?

For straightforward PIP claims that are being processed properly, you may not need an attorney. However, if your claim is denied, your benefits are delayed, or you believe you're not receiving the full benefits you're entitled to, consulting with an experienced Melbourne car accident attorney is advisable.

If your injuries appear to meet the serious injury threshold or your damages will clearly exceed the PIP limits, it's particularly important to consult with an attorney early in the process. At Douglas R. Beam, P.A., we handle all personal injury cases on a contingency fee basis. This means you don't pay attorney fees unless we win your case, allowing you to get the legal representation you need without upfront costs.

If Florida changes to an at-fault system, will my existing PIP policy still cover me?

If Florida were to switch to an at-fault system in a future session, there will likely be a transition period during which existing policies remain in effect. The new requirements would typically apply when you renew your policy after the law's effective date. Insurance companies would be required to notify you about changes to your coverage and any new requirements before your policy renewal.

Key Takeaways

- Florida's no-fault system requires drivers to carry $10,000 in PIP coverage, which pays for your own injuries regardless of who caused the accident.

- You must seek medical treatment within 14 days of an accident to qualify for PIP benefits.

- To sue for pain and suffering damages, you must meet Florida's "serious injury threshold" by suffering permanent injury or significant scarring.

- Under Florida's modified comparative negligence law, you cannot recover damages if you are more than 50% at fault for the accident.

- Florida's legislature has repeatedly tried to eliminate the no-fault system, most recently in the 2026 session, but every repeal bill has failed, so the no-fault system remains in place.

Understanding Florida's no-fault insurance system is essential for every Melbourne driver, especially as lawmakers periodically revisit the system. If you've been injured in an accident, knowing how these laws apply to your specific situation can make a significant difference in your recovery—both physically and financially.

At Douglas R. Beam, P.A., we handle all personal injury cases on a contingency fee basis. This means you don't pay attorney fees unless we win your case, allowing you to get the legal representation you need without upfront costs.

Contact our experienced Melbourne car accident attorneys for a free consultation to understand how Florida's insurance laws apply to your specific situation.

Please remember, this article provides general information based on Florida law and is intended for educational purposes only. It does not constitute legal advice and should not be relied upon as such. Every case is unique, and the information here may not apply to your specific circumstances. Reading this article does not create an attorney-client relationship. For advice tailored to your situation, please consult with a qualified attorney.

Sources and Further Reading

- Florida Highway Safety and Motor Vehicles - Insurance Requirements

- Florida Statutes - Motor Vehicle No-Fault Law

- Florida Statutes - Tort Exemption

- Florida Statutes - Comparative Fault

- Florida Senate - SB 1256 Bill Information

- Florida Phoenix - House Panel Votes on No-Fault Insurance

- Florida Supreme Court Decision - Progressive v. Florida Hospital Medical Center

- Jimerson Law - Florida Tort Reform and Comparative Negligence

- ABC Action News - No-Fault vs. At-Fault Insurance Impact

- FL Senate Bill 522 (2026)

- FL House Bill 769 (2026)

Not Sure What To Do Next? We Can Help – Fast & Free.

.webp)

Worried About Your Injury Case?

We'll Review It - Free

Don’t miss an article

Florida law, local insights, and the occasional dog pic.

Delivered straight to your inbox.

More articles

Browse all articles

.png)

.png)

Free Case Review

Get a complimentary review of your case