Understanding Florida Car Accident Settlements: A Complete Guide

Learn how Florida car accident settlements work after 2023 law changes. Understand no-fault insurance, settlement factors, & your rights in Brevard County.

.webp)

Riley Beam

- Florida's no-fault system requires PIP coverage but allows additional claims for serious injuries beyond your own insurance limits.

- 2023 law changes created a 50% fault bar and reduced lawsuit deadlines to just two years from accident date.

- Settlement amounts vary dramatically based on injury severity - never use general statistics to estimate your specific case value.

Worried About Your Injury Case? We'll Review It - Free!

How Florida's Car Accident Laws Work

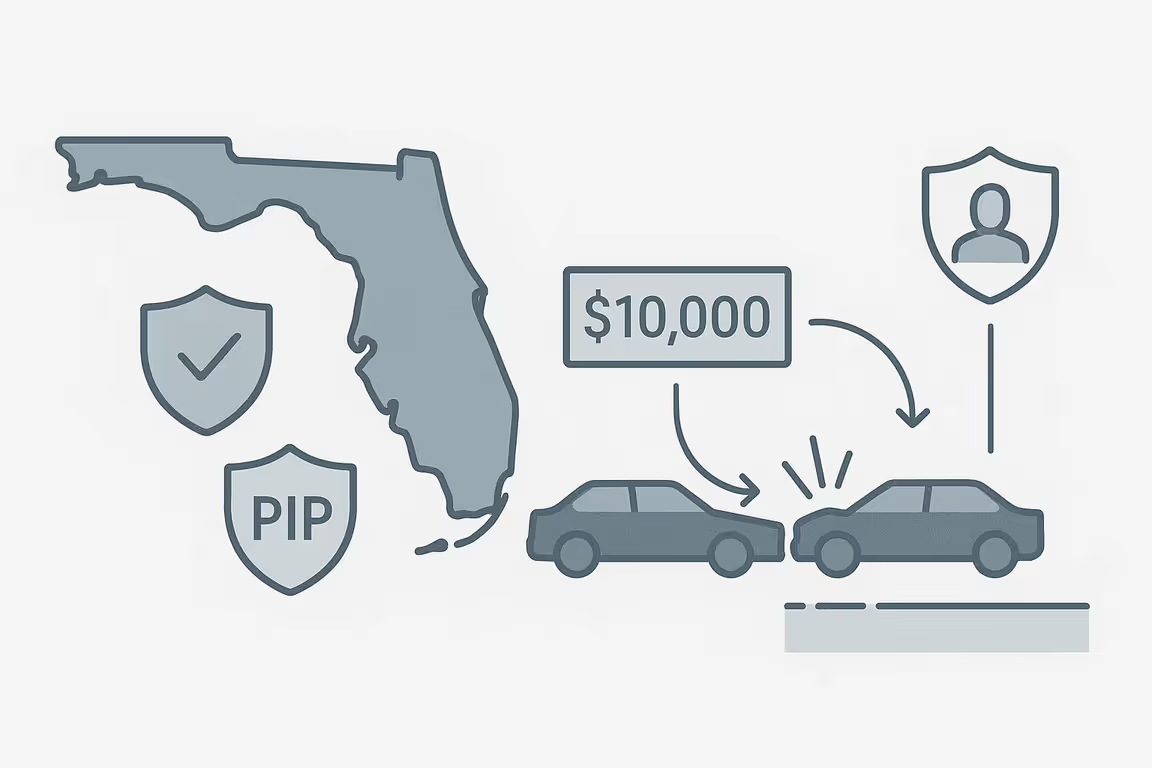

When you're involved in a car accident in Florida, understanding how settlements work can feel overwhelming. Florida operates differently from many other states because of its unique no-fault insurance system, which affects how accident claims are handled and what compensation you might receive. Florida's car accident laws are built around what's called a "no-fault" insurance system. This means that after an accident, your own insurance company initially pays for certain expenses, regardless of who caused the crash. Understanding this system is crucial because it affects every aspect of how settlements work in our state.

Under Florida law, all drivers must carry Personal Injury Protection (PIP) coverage as part of their auto insurance policy. This coverage typically provides up to $10,000 in medical benefits and disability benefits to pay for immediate medical expenses and a portion of lost wages after an accident. The key point is that PIP pays these benefits regardless of who was at fault for the accident.

However, PIP coverage has limitations. It doesn't cover all your medical expenses, and it provides only partial wage replacement. More importantly, PIP doesn't compensate you for pain and suffering, which can be a significant part of your damages in a serious accident.

You can pursue additional compensation beyond your PIP benefits when your injuries meet certain thresholds. These include cases involving permanent injury, significant scarring or disfigurement, or death. In these situations, you may be able to file a claim against the at-fault driver's insurance company for damages that exceed your PIP coverage.

If you're dealing with a car accident in Melbourne or anywhere in Brevard County, Melbourne car accident attorneys who understand Florida's unique system can help explain how these laws specifically apply to your situation. The interaction between PIP coverage and additional liability claims can be complex, and recent changes to Florida law have made the landscape even more complicated.

Recent Changes to Florida Law (2023-2024)

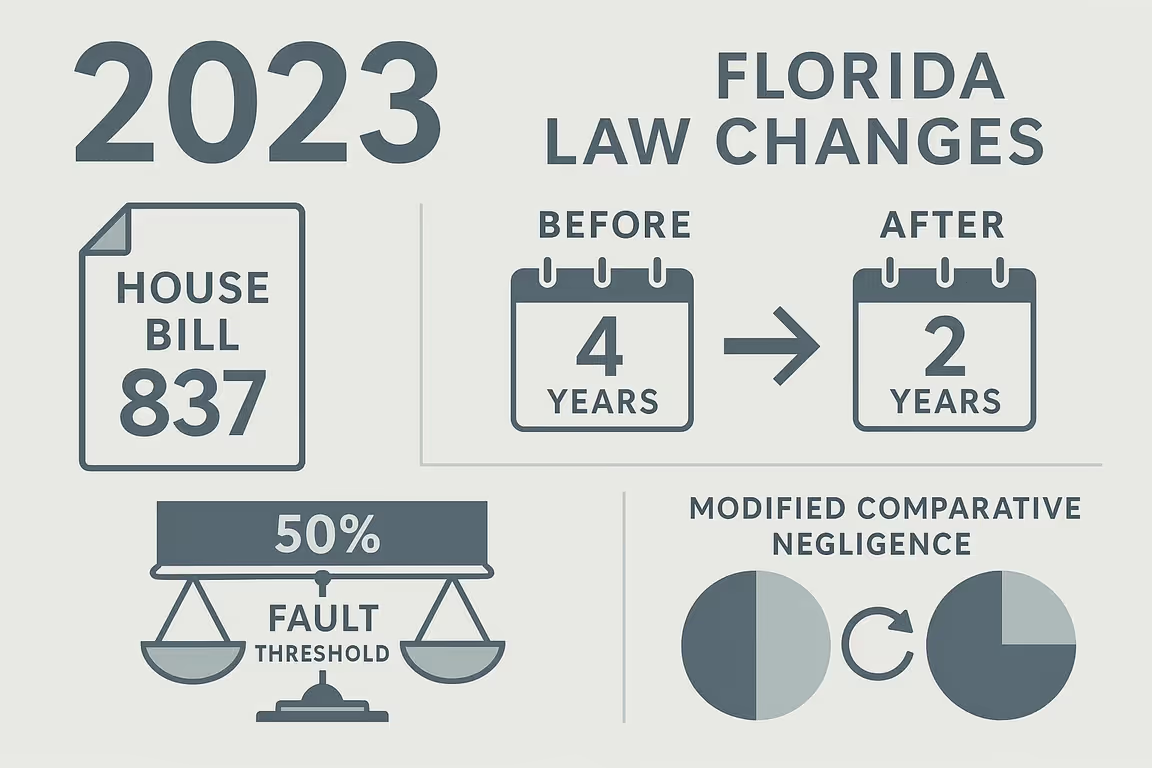

Florida's personal injury landscape changed significantly in March 2023 with the passage of House Bill 837, a comprehensive tort reform package. These changes directly affect how car accident settlements work, and understanding them is important for anyone involved in a recent accident.

One of the most significant changes involves what's called "comparative negligence." Previously, Florida followed a "pure comparative negligence" rule, which meant you could still recover some compensation even if you were mostly at fault for an accident. Now, Florida operates under "modified comparative negligence," which means if you are found to be more than 50% at fault for the accident, you cannot recover any compensation from the other driver.

For example, if a court or insurance company determines that you were 60% responsible for the accident and the other driver was 40% responsible, you would not be eligible to receive any settlement money from the other driver's insurance company. This is a significant change that can affect settlement negotiations and the value of claims.

Another critical change is the reduction of the statute of limitations for personal injury claims. Previously, accident victims had four years to file a lawsuit. Now, that deadline has been reduced to just two years from the date of the accident. This shorter timeframe means it's more important than ever to act promptly if you're considering legal action.

These changes generally make it more challenging for people who bear significant fault to recover damages. Insurance companies are aware of these new rules and may use them in settlement negotiations. However, experienced attorneys who have adapted to these changes can still effectively advocate for clients within this new legal framework.

The tort reform also affected other aspects of personal injury law, including how attorney fees are calculated and when they can be recovered. While these changes create new challenges, they don't eliminate your right to fair compensation if you've been injured due to someone else's negligence.

Understanding Settlement Amounts - General Information

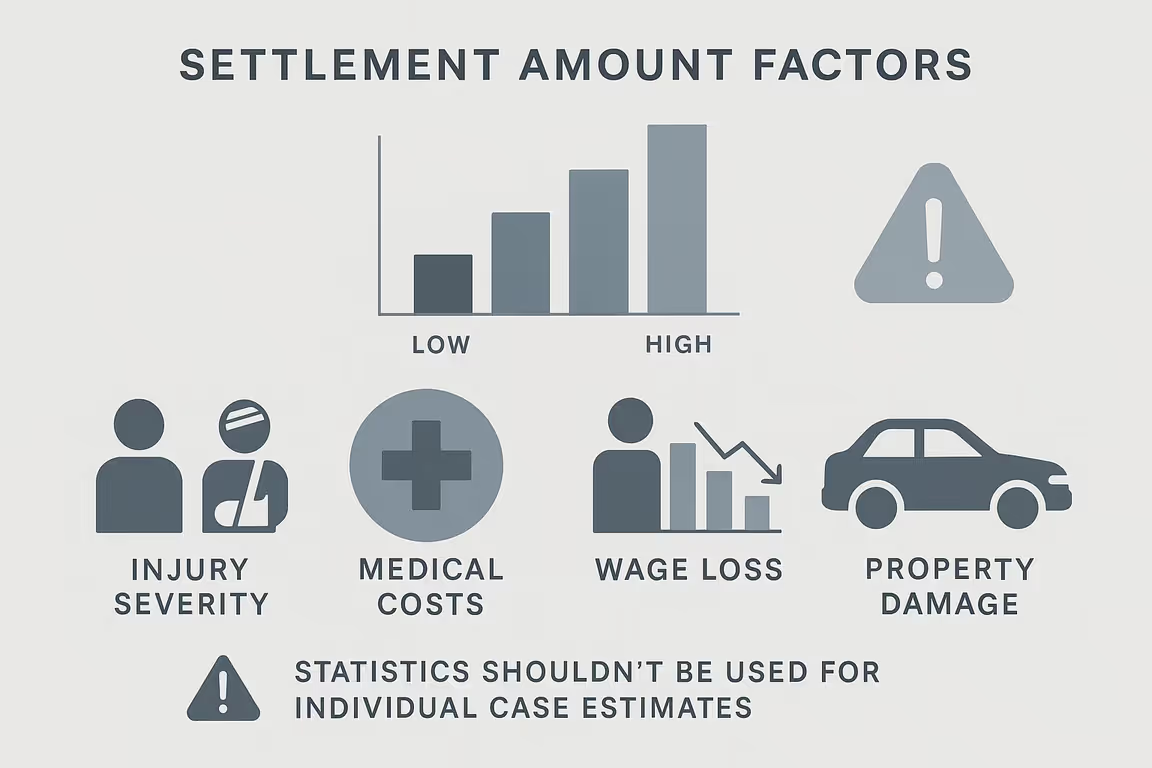

When people ask about "typical" car accident settlement amounts in Florida, it's important to understand that every case is genuinely different. While we can provide general information about settlement ranges, these numbers should never be used to estimate what any specific case might be worth.

Nationally, car accident settlements average around $37,248, but this figure can be misleading because it includes everything from minor fender-benders to catastrophic injury cases. In reality, settlements can range from a few thousand dollars for minor soft tissue injuries to hundreds of thousands or even millions of dollars for severe injuries or wrongful death cases.

Several factors significantly influence settlement amounts in Florida car accident cases. The severity of your injuries is typically the most important factor. Cases involving broken bones, traumatic brain injuries, spinal cord injuries, or permanent disabilities generally result in higher settlements than cases involving minor cuts, bruises, or temporary soft tissue injuries.

Medical expenses play a crucial role in settlement calculations. This includes not just your immediate medical bills, but also future medical care you may need related to your injuries. Lost wages are another significant component - both the income you've already lost due to your injuries and any reduction in your future earning capacity.

In Florida's no-fault system, your PIP insurance typically covers initial medical bills up to $10,000, which can affect how additional damages are calculated. If your medical expenses exceed your PIP coverage, or if you have permanent injuries, the settlement might include compensation for these excess costs.

Pain and suffering damages can also be substantial in qualifying cases, though they're often the most difficult to quantify. Unlike medical bills or lost wages, which have specific dollar amounts, pain and suffering is more subjective and depends on factors like the nature of your injuries, how they've affected your daily life, and how long your recovery is expected to take.

Property damage is usually handled separately from personal injury claims. While car repairs or replacement are typically straightforward to calculate, they don't necessarily reflect the severity of injuries or potential settlement value for personal injury claims.

For residents of our area, Brevard County personal injury lawyers understand the local factors that can influence settlement negotiations, including how local courts tend to handle these cases and the approaches of insurance companies operating in our region.

Important Deadlines and Timeline Considerations

Time is critical in Florida car accident cases, and recent changes have made certain deadlines even more important. The most significant deadline you need to understand is the statute of limitations for filing a personal injury lawsuit.

As of 2023, you have two years from the date of your car accident to file a personal injury lawsuit in Florida courts. This represents a significant reduction from the previous four-year deadline. This deadline is firm - if you miss it, you generally lose your right to pursue compensation through the court system, even if you have a strong case.

It's important to note that the statute of limitations applies to filing a lawsuit, not to settling your case. Many car accident cases settle through negotiations with insurance companies without ever going to court. However, the lawsuit deadline still matters because it affects your negotiating position. Insurance companies know that once the deadline passes, they no longer face the potential risk of a court judgment.

The settlement process itself typically takes several months to over a year, depending on the complexity of your case. Simple cases with clear fault and minor injuries might settle relatively quickly, while cases involving serious injuries, disputed fault, or complex medical issues can take much longer.

Several factors affect the timeline of settlement negotiations. First, you generally shouldn't settle your case until you've reached what doctors call "maximum medical improvement" - the point where your condition has stabilized and doctors have a clear picture of your long-term prognosis. Settling too early can mean accepting less compensation than you deserve if your injuries turn out to be more serious than initially thought.

Insurance companies also have their own deadlines for PIP claims that are much shorter than the lawsuit deadline. You typically need to report your accident and submit PIP paperwork within 30 days of the accident, and you have specific timeframes for submitting medical bills and other documentation.

Documentation of your injuries and treatment should begin immediately after your accident. This includes keeping records of all medical appointments, treatments, medications, and how your injuries affect your daily life. The more comprehensive your documentation, the stronger your position in settlement negotiations.

Douglas R. Beam P.A. has been handling time-sensitive aspects of Florida accident cases since 1988, and our experience with thousands of cases has shown how crucial it is to begin the legal process promptly while still allowing sufficient time for a complete medical recovery.

If you need guidance on what steps to take immediately after an accident, our article on what should I do after a car accident provides detailed information about protecting your rights from day one.

Frequently Asked Questions About Florida Car Accident Settlements

How long does it take to settle a car accident case in Florida?

Settlement timelines vary widely depending on several factors. Simple cases with clear fault and minor injuries might settle within a few months, while complex cases involving serious injuries or disputed fault can take a year or more. The process typically involves several stages: initial medical treatment and documentation, insurance claim filing, investigation by insurance companies, negotiations, and potentially mediation or litigation if an agreement can't be reached.

Several factors affect the timeline. If liability is disputed - meaning there's disagreement about who caused the accident - this can significantly extend the process. The severity of your injuries also matters; you generally shouldn't settle until you've reached maximum medical improvement and understand the full extent of your damages. Insurance company cooperation varies as well; some companies make reasonable settlement offers quickly, while others may require more intensive negotiations.

What if I was partially at fault for the accident?

Under Florida's modified comparative negligence rule that became effective in 2023, your ability to recover compensation depends on your percentage of fault. If you are found to be 50% or less at fault, you can still recover compensation, but it will be reduced by your percentage of fault. However, if you are determined to be more than 50% at fault, you cannot recover any compensation from the other driver.

For example, if your total damages are $50,000 and you're found to be 30% at fault, you could potentially recover $35,000 (your damages reduced by your 30% fault percentage). This is a significant change from Florida's previous law, which allowed recovery even if you were more than 50% at fault, with compensation simply reduced by your fault percentage.

Fault determination can be complex and often involves investigation of the accident scene, review of police reports, witness statements, and sometimes accident reconstruction experts. Insurance companies and attorneys may have different opinions about fault percentages, which is why having experienced legal representation can be important in these situations.

Do I have to accept the first settlement offer?

No, you are not required to accept any settlement offer from an insurance company. Settlement offers are negotiations, and you have the right to reject offers that don't adequately compensate you for your damages. However, there are important considerations to keep in mind.

First, evaluate whether the offer adequately covers all your damages, including medical expenses (both past and future), lost wages, property damage, and pain and suffering in qualifying cases. Often, initial offers from insurance companies are lower than what a case might ultimately be worth, particularly before all medical treatment is complete.

Consider the strength of your case, including clear evidence of fault and well-documented injuries. Also consider the costs and time involved in continued negotiations or potential litigation. Sometimes a reasonable settlement offer might be preferable to the uncertainty and expenses of a trial, while other times it may make sense to continue negotiations.

Remember that once you accept a settlement and sign a release, you typically cannot reopen the case later if you discover additional injuries or damages. This is why it's generally advisable not to settle until your medical condition has stabilized.

What costs are typically covered in a car accident settlement?

Car accident settlements can include several types of compensation, depending on the circumstances of your case. Medical expenses are typically the largest component, including hospital bills, doctor visits, prescription medications, physical therapy, and necessary future medical care related to your injuries.

Lost wages include income you've already lost due to your inability to work because of your injuries. In more serious cases, settlements might also include compensation for reduced future earning capacity if your injuries permanently affect your ability to work.

Property damage to your vehicle is usually handled separately but can be part of an overall settlement. This includes repair costs or the replacement value of your car if it was totaled.

In cases that meet Florida's injury threshold, settlements can also include compensation for pain and suffering, which addresses the physical discomfort and emotional distress caused by your injuries. This element is often the most difficult to quantify and can vary significantly based on the nature and extent of your injuries.

How do I know if I need an attorney?

While not every car accident case requires an attorney, legal representation becomes more important in certain situations. Consider consulting with an attorney if you've suffered serious injuries, if fault for the accident is disputed, if the insurance company is denying your claim or offering what seems like inadequate compensation, or if you're unsure about how Florida's laws apply to your situation.

An attorney can be particularly valuable when dealing with complex medical issues, when multiple parties are involved in the accident, or when you're facing pressure to settle quickly before you understand the full extent of your injuries. Attorneys experienced in Florida car accident law understand how recent legal changes affect cases and can help navigate the complexities of both PIP claims and liability claims.

Many personal injury attorneys work on a contingency fee basis, meaning they only get paid if they recover compensation for you. This can make legal representation accessible even if you're facing financial stress due to your accident.

Understanding Florida's car accident settlement process can help you make informed decisions about your case. However, given the complexity of Florida law and the significant changes that have occurred recently, consulting with experienced legal professionals can provide valuable guidance tailored to your specific situation.

If you have questions about a car accident in Melbourne or Brevard County, contact Douglas R. Beam P.A. for a consultation to discuss your specific situation. Our firm has been serving the Brevard County community since 1988, and our experience with over $1 billion in verdicts and settlements has helped thousands of clients navigate the complexities of Florida's personal injury law.

This article provides general information and is not a substitute for legal advice. Laws can change, and the details of your situation matter. For personalized guidance, please contact a qualified Florida personal injury attorney.

Not Sure What To Do Next? We Can Help – Fast & Free.

.webp)

Worried About Your Injury Case?

We'll Review It - Free

Don’t miss an article

Florida law, local insights, and the occasional dog pic.

Delivered straight to your inbox.

More articles

Browse all articles

.png)

.png)

Free Case Review

Get a complimentary review of your case